Step into retirement with confidence through proper planning

The Gap Between Retirement Income and Needs

To step off the ledge from working and making a regular income to retiring and not having an income, is scary. Once you make that leap into retirement, it is difficult to go back, if even possible.

At retirement, you’ll likely get some government pension income (like the CPP Retirement pension and OAS). Some people might also have a pension from their work and/or rental income from a rental property. We’ll call these amounts your retirement income.

If your planned spending is greater than your retirement income, your savings needs to fill that gap. The challenge is how to invest your money to fill that gap over your lifetime.

Stuffing Money Under the Mattress

Stuffing your life savings into a mattress (or into a Chequing account) faces a loss of purchasing power every year due to inflation. And if you don’t have enough, every year your mattress cash depletes. Eventually the mattress money is gone and you face the dilemma of going back to work, being dependent on your children, or being dependent on the government.

A step up from the mattress stuffing is that of buying bank term deposits or GICs where such funds are not tax sheltered and where taxes take a good chunk out of returns.

Let’s assume you can buy a GIC at 5.0%. If the resulting interest income is taxed at say 40%, you will lose 2% of the return to tax. If inflation is 3%, then the purchasing power of your money just keeps up with inflation. Your living needs have likely increased by inflation and that risk of outliving your money still remains.

Alternatively, if you can invest in GICs in a tax sheltered account, like a Tax Free Savings Account, where you end up with an actual 2% return after 3% inflation and no taxes. So this type of safe investment in such an account can make sense if you can fill your holes with a 2% real return. Having such investments do have a place in a portfolio. They can help you be opportunistic when the market is down to buy

Investing for Growth

Investing for growth also works well in pre-retirement, where you are not drawing from your portfolio. Your needs are met from your working income. But in retirement, we are putting some stress on your portfolio to help fund your needs.

To fund the difference between retirement income and needs, you could put part of your life savings into the stock market. The hope is that you can make a good return to more than fund the gap between retirement income and needs.

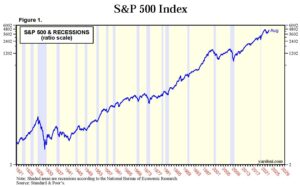

The problem is that the stock market is volatile. It does not generate a consistent return month to month and year to year. Economic business cycles eventually end in a recession every seven to ten years. And stocks tend to decline during such periods (see chart below).

cheap.

But what if 2% isn’t enough or we can’t put all our money into such a tax friendly place (or a low income person’s hands)?

Source: Stock Market Indicators: S&P 500 Recession Cycles, August 31, 2023 by Dr. Ed Yardeni.

Where you choose to invest in stocks with the aim of a high return, this may be a solution of using the growth to fund the gap. But for this to work, the percentage of the portfolio that is drawn needs to be modest. Or, we need to have flexibility to reduce draws by deferring non-necessities in bad markets. By reducing the amount of investments to sell when they are down, we hope the portfolio will have a greater chance to recover.

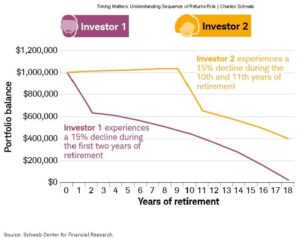

Where one experiences a sequence of negative returns, eating capital at the same rate can result in outliving money even if returns improve in the future.

Charles Schwab provides hypothetical example illustrating the impact of a negative sequence of returns. Both hypothetical investors had a starting balance of $1 million, took an initial withdrawal of $50,000, and increased withdrawals 2% annually to account for inflation. Investor 1’s portfolio assumes a negative 15% return for the first two years and a 6% return for years 3–18. Investor 2’s portfolio assumes a 6% return for the first nine years, a negative 15% return for years 10 and 11, and a 6% return for years 12–18. The illustration does not reflect expenses, fees, or taxes.

Source: www.schwab.com/learn/story/timing-matters-understanding-sequence-returns-risk

There are no guarantees that your portfolio will achieve a certain level of return. There have been periods where the market has delivered poor returns for several years. What if the stock market goes through another protracted recession or a period of low growth and low market returns so that you end up eating more capital than planned in the early years?

An alternative approach to filling the gap

With some googling, you’ll comes across the topic of risk adjusted returns in retirement when one draws on their portfolio (some label this as terminal wealth funding).

The idea is that, during a period of regular draws, a lower return lower volatile portfolio can be superior to a higher return higher volatile portfolio. The key is to maximize returns after but taking risk into consideration (also known as risk adjusted returns).

Managing risk is also important to allow us to psychologically stick with your investing strategy during the down periods.

How do we Find Good Returns with Relatively Low Risk?

James O’Shaughnessy wrote a book called, “What Works on Wall Street”. This book provides us with the answers we seek.

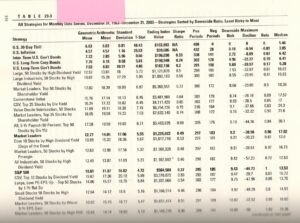

In the third edition, Table 23-3 provides a ranking of strategies from least risky to most for the 40 year period of 1963 to 2003.

Source: What Works on Wall Street by Jim OShaughnessy, 3rd Edition

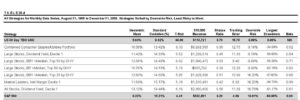

In the fourth edition, Mr. O’Shaughnessy provides the ranking of downside risk from least risky to most for the period of Aug 31, 1965 to Dec 31, 2009 in Table 28.4 (we include only part of the table of the strategies with better downside risk than the S&P500 Index).

Source: What Works on Wall Street, Supplemental Table to the 4th Edition; DIVY = Dividend yield;

The conclusion I draw from these studies is that over 80 years, large companies with high dividend yields have been less risky than the S&P 500 Index and have also provided better returns (see the Geometric Mean; also known as compounded return).

So for stocks, we need to buy a sufficiently large enough group of stocks to increase the odds of achieving strategy returns (at least 20). The more stocks we buy, our capital becomes more stable as well as the dividend income stream.

An interesting point about a company that pays a dividend is that a company usually chooses a dividend rate that they figure they can sustain over time. Should a company not be able to pay the dividend, its share price can be expected to drop substantially. So the dividend may be considered a more stable return on investment as opposed to relying on the share price to regularly increase.

Spend only income and not sell depressed investments

Should we only spend the dividends, thereby leaving the stocks intact, those companies may continue paying those dividends into the future. We might also seek extra assurance of the dividend stability by selecting large stable businesses that earn enough to pay the dividend (this helps us manage longevity risk).

The earnings of the companies that were retained (not paid out as dividends) helps fuel the portfolio towards strategy total returns. Companies may use the retained earnings to increase dividends or grow the business and increase earnings. And that helps us to keep up with inflation.

Where the gap can be filled with only dividend income, then we have a potentially sustainable solution. And we no longer are dependent on the stock market to rise to be able to fund our living needs.

But what about taxes?

When we spend money, we spend after-tax income. For Canadians, if our dividends were generated from Canadian listed corporations, such dividends may qualify for the dividend tax credit. This credit can materially increase the dividend income advantage when we compare to investments that generate interest income, foreign dividends and capital gains.

But what about investment risk and portfolio volatility?

Let’s be clear that we are not promoting anyone putting all of their money into stocks. Most people, even very experienced investors, cannot stomach the volatility of such a portfolio.

Rather only a portion of a properly diversified portfolio would contain large dominant dividend paying stocks with a good dividend yield that also earn enough to pay that dividend.

We need to have at least 6 months of living needs plus an emergency fund in cash or in liquid fixed income investments. This helps to smooth out the funding of monthly withdrawals as dividends are normally paid on a quarterly basis. We would also need other types of investments like bonds and preferred shares to manage portfolio stability and lessen portfolio capital fluctuations.

Portfolio volatility needs to be at a level that you can stomach. If not, there’s a risk that the portfolio is taken apart. And such a time would typically be when these type of investments are down.

Summary

Our goal for our client is to fill the gap for our client every year for their lifetime and that of their spouse.

Consider one retired couple that have government pensions and receive $100,000 in Canadian eligible dividends. With planning their tax equity, they report $50,000 each of dividends. As a result, they pay little to no income taxes due to their basic credit, age credit and dividend tax credit.

As long as they do not spend any of the capital, the portfolio should be able to generate that income each year as long as they live.

The stress of the market ups and downs are no longer an issue as they are not dependent on the market to continually rise to meet their needs.

And when they pass away, the capital can pass to their children to take care of their needs.

I hope that this article is insightful and helpful. If you would like to explore building an income portfolio, please call or email me.

FAQ: Retirement Income Planning

Why is the transition into retirement considered financially risky?

Retiring means giving up a regular income from work. If your spending is more than your retirement income (like CPP, OAS, pensions, or rental income), your savings must cover the gap. Poor planning can lead to outliving your money.

Is keeping retirement savings in a chequing account or under the mattress a good idea?

No. While this avoids investment risk, it exposes you to inflation risk and loss of purchasing power. Eventually, you may deplete your savings if they don’t grow.

Are GICs a good retirement investment?

GICs can be useful, especially in tax-sheltered accounts like a TFSA. However, in taxable accounts, high taxes and inflation may reduce their real returns. A 5% GIC taxed at 40% only yields 3%, and if inflation is 3%, your return is effectively 0%.

Can you rely on the stock market to fund retirement?

Stocks offer growth potential, but come with volatility. Market downturns can be harmful if you’re withdrawing money during a bad sequence of returns. Having flexibility to reduce withdrawals in down years can help.

What is ‘sequence of returns’ risk?

It refers to the order in which investment returns occur. Taking withdrawals during early negative-return years can permanently harm your portfolio, even if the market recovers later.

What kind of investment strategy helps reduce risk in retirement?

Low-volatility, dividend-paying stocks (especially Canadian companies) can provide stable income. Combined with a diversified portfolio, this reduces the need to sell assets in down markets.

What is the benefit of dividend-paying stocks in retirement?

Dividends offer a more stable source of income compared to relying on share price increases. Large companies with consistent earnings and dividends help preserve capital and support longevity.

What’s the tax advantage of Canadian dividends?

Eligible dividends from Canadian companies qualify for the dividend tax credit, which can significantly reduce taxes owed—sometimes to zero for retirees with modest income needs.

How much cash should be in a retirement portfolio?

At least 6 months of living expenses plus an emergency fund should be held in cash or liquid fixed income. This allows stability and avoids forced sales during market dips.

- Cash Management is King - October 19, 2025

- Disability Insurance - September 17, 2025

- Representation Agreement - August 14, 2025