Stock Picks and Review for June 2022

Today is June 16, 2022, and it’s time for some new stock picks and market commentary. As always, I’ll start by reviewing the picks I had this time last year.

June 2021

Last June, I recommended Meta Financial Group, which was down 28.8% since this time last year; Dollar General (NYSE: DG), which was up 13.7% since this time last year, including dividends; and Kirkland gold, which merged with Agnico-Eagle Mines (NYSE: AEM) in February of this year. The combination of holding Kirkland and then Agnico-Eagle over the last year would have resulted in a return of -7.9%. The average of these three was -7.7%, which compares to -12.2% for the world markets, as represented by the MSCI World Index ETF (URTH) in US Dollars, including dividends.

Analysis of Today’s Markets

We are now in a highly unusual situation. We haven’t experienced anything like it, I think, since probably the ‘80s. We have inflation, higher inflation that we haven’t seen since the beginning of the 1980s and rising interest rates. There’s a lot of speculation that we’re going to have a recession. I’m going to comment on this and what can happen during such times. I’ll also discuss the possibility of stagflation, where we have inflation and slow economic growth.

Gauging an Economic Recession

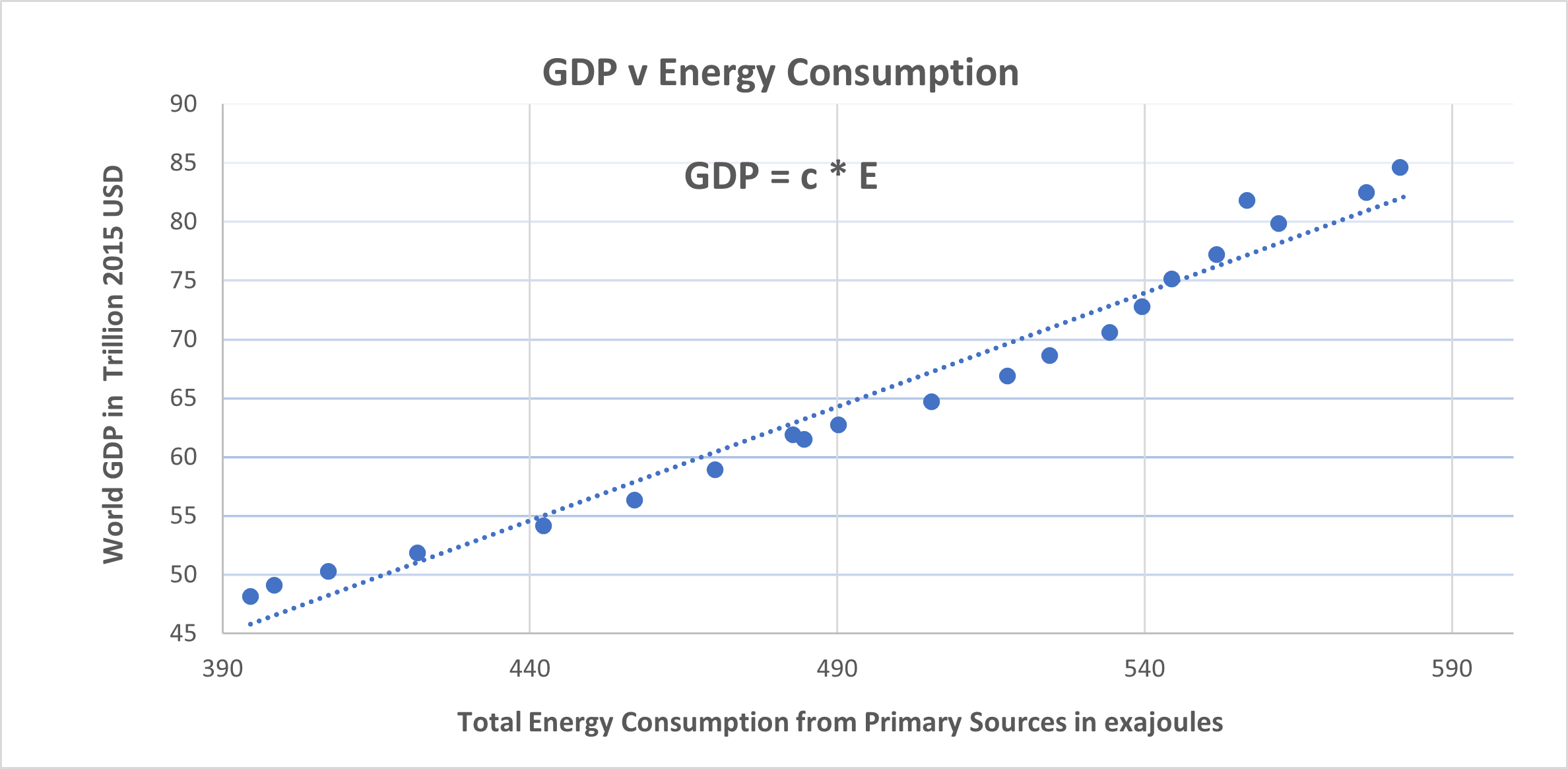

My view on the possibility for recession is that it’s quite likely. The reason is probably not just “the Fed and other banks raising rates”, even though that’s going to be the immediate explanation that everybody will have. A simpler explanation may be that the world output as measured by GDP, is a function of energy consumed. It takes more energy to make more stuff. It’s as simple as that.

GDP and Energy Consumption

Energy consumption (from primary sources) is able to explain and predict GDP with almost 100% accuracy. It is eerily accurate:

GDP = c * E

Worldwide GDP is equal to: an energy conversion efficiency coefficient c (that measures the efficiency of our ability to convert energy into things) times E, the energy that we actually use.

And energy efficiency over time improves because we’re getting better at making more stuff using less energy. Think for example, LED light bulbs using less energy than the old incandescent bulbs.

We still need more energy, though. And we’ve had a massive underinvestment in the industry. This is especially true for the conventional oil and gas business over the last 15 years, and particularly during 2020. During the lockdowns, the price of oil worldwide had dropped to really really low levels. So, companies responded by slashing their investment expenditure to next to nothing.

Money that’s being invested now in the sector will take four to six years before it results in increased oil and gas production. And it’s not easy to replace the energy growth that’s being lost from these conventional sources by the renewable sources, like wind and solar, even things like nuclear. Even those things take a long time to bring to market.

The world population is growing and our energy production is not able to keep up with the demand growth. Therefore, there is a decent chance that we’re going to be in a recession for the next year or two until we get more energy from all sources to satisfy the needs of the world economy.

Portfolio Recommendations

As a brief aside, I should say that for the first time in almost 14 years, we are adding GICs (Guaranteed Investment Certificates) into client portfolios. We are getting rates of around 4.5%, which we haven’t seen in a very long time.

Regarding stock picks, given the uncertain economic environment that we are in, my thinking now is to concentrate on quality, larger companies and companies that pay dividends. I believe they’re likely do better in an uncertain environment than smaller companies.

Verizon Communications (NYSE: VZ)

Ideally, I like larger companies with a dividend yield for over 3.3%, which is the current yield on the 10 year note. A lot of these stocks are trading at reasonable valuations. They should also have the ability to grow if they don’t pay all their earnings out in dividends. So, a payout ratio of less than 60% or so is good. One such example is Verizon Communications (NYSE: VZ). I believe they are the largest cell carrier in the world. I think it has a very good dividend yield around 5.2%, payout ratio is around 50%, and valuation is reasonable. So that would make a good place to have some money.

Devon Energy Corp (NYSE: DVN)

A second pick would be one that’s an inflation hedge in case we’re continuing to see inflation going forward. I was thinking about the 1970s and the possibly similar conditions as we are seeing now. Stocks did okay then, but the majority of the return came from dividends. In fact, more than 50% of total returns came from dividends. Another factor to consider was that energy was about the only sector that did well during that time – really well. Precious metals performed just as well, but precious metals were very undervalued back then and they’re probably not undervalued now.

With that in mind, a large cap energy stock makes sense, so I picked Devon Energy Corp (NYSE: DVN). With Devon, we have everything that I mentioned we need with regards to entering this kind of environment. They have a dividend yield of 5.3%, an inflation hedge and hopefully a decent valuation. Valuation remains to be seen because if we go into recession and there’s demand destruction, perhaps energy companies will not do as well. Nonetheless, the future is always uncertain and it’s good to be well-diversified.

Cisco Systems (NASDAQ: CSCO)

If things are not as bad as most people anticipate, technology companies should do reasonably well. Here I’m sticking with a quality tech stock pick: Cisco Systems (NASDAQ: CSCO). Cisco was one of the darlings of the 1990s. Since then, it’s been more of a mature business and now the valuation is reasonable. They also pay a dividend of 3.4%. So, it has the quality, has the scale, and ideally has the ability to withstand the recession.

That’s a kind of technology company that we feel comfortable owning. If things don’t go as badly as anticipated, though, the more “growthier” technology companies will do a lot better. However, this is probably not the time to be chasing the high growth names.

We’re Here to Help

So if you’d like a second opinion about your portfolio, diversification,, or whether these stocks fit in your portfolio, don’t hesitate to give us a call. Thank you and have a great day.

- Stock Picks for June 2026 - June 19, 2026

- Top ideas for new money for 2026 - January 12, 2026

- Stock Picks for January 2026 - January 7, 2026